The Recovery in Commercial Aviation

- Alviss Analysts

- May 4, 2021

- 3 min read

Updated: May 24, 2021

To date:

We all know that COVID-19 created an adverse effect on our ability to fly, in fact it created the largest downturn in commercial aircraft passenger traffic in history. The impact of this was a 60% total decline in world passengers in 2020 from 2019 figures according to the International Civil Aviation Organisation (ICAO).

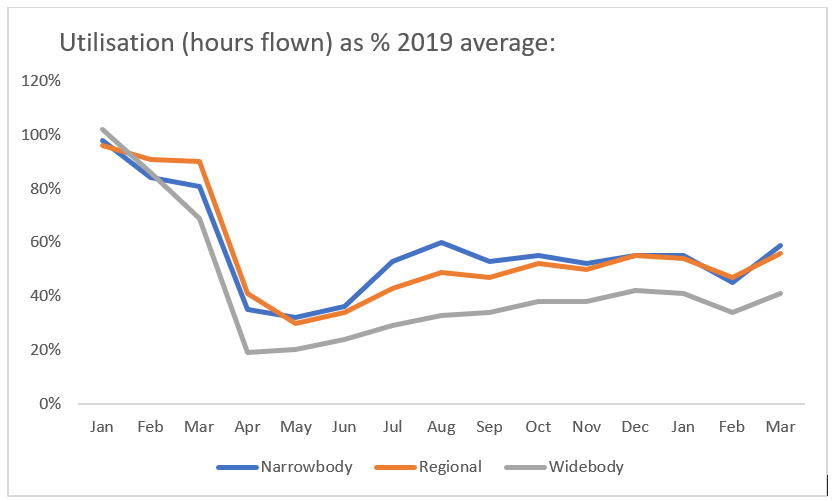

This decline in passenger figures was reflected in the drastic reduction in flying hours of the commercial aircraft fleet, with widebody (twin aisle) jets disproportionally affected by the virus as international travel stalled and nations closed their borders. As of the time of writing there has been some recovery since the low point in April 2020, however total commercial aircraft utilisation (in terms of hours flown) has trended at 50-60% of 2019 levels for the past six months.

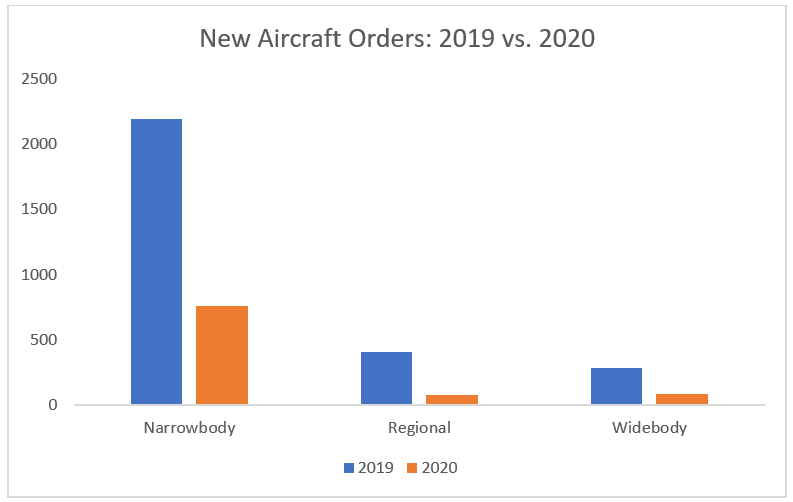

This market downturn impacted airline fleet plans, with several operators choosing to retire older, less fuel-efficient platforms whilst passenger demand was low. The lack of passengers had a consequent impact on airline finances, which they partly tried to balance by pushing back planned aircraft deliveries and reducing new orders. This led to an overall drop in orders of 68% year-over-year from 2019 across the commercial fleet.

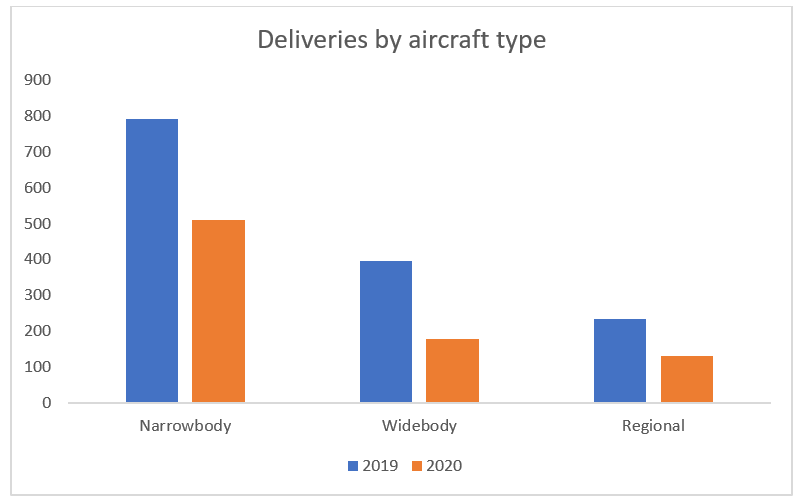

This drop in orders led original equipment manufacturers (OEM’s) to reduce their production rates to maintain longevity in their order books. These deferrals in deliveries and the drop in production were the largest contributing factors to a large decrease in aircraft deliveries in 2020 (with the 737 Max re-certification and practical delivery issues relating to the pandemic also being contributing factors):

Despite this reduction in production rates the firm order book for the commercial aircraft fleet has still declined 9% overall from the end of 2019.

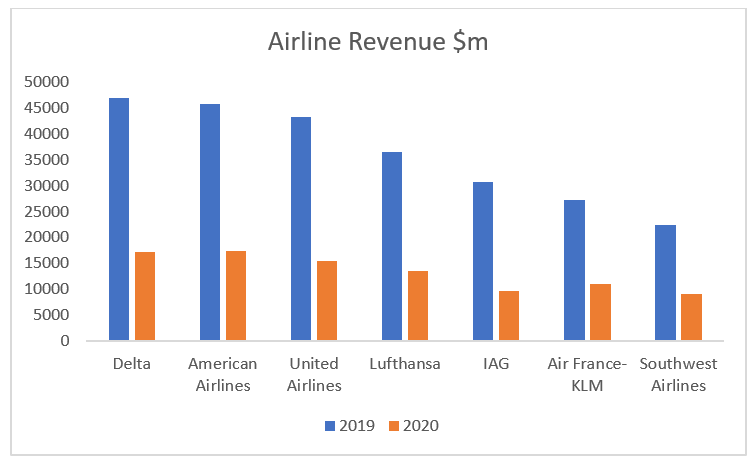

The financial impact of the virus on operators has been devastating with the top seven airlines in the world by sales experiencing a combined drop of $160b in revenue and a loss of $34b in EBITDA.

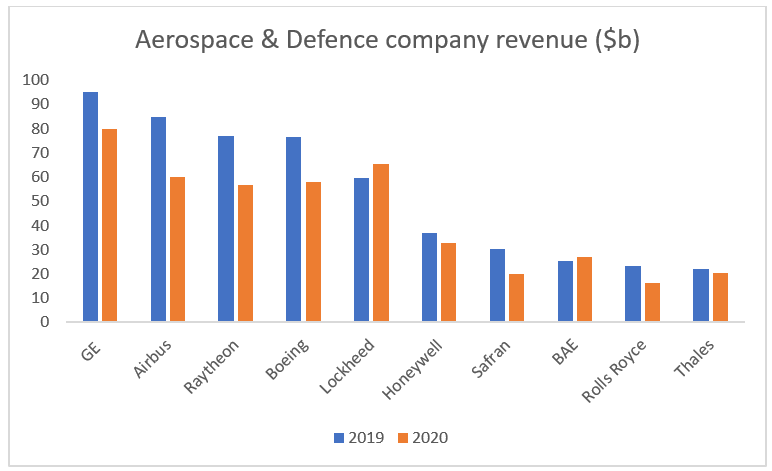

This financial loss has also been experienced by the airframers and manufacturing supply chain of the aerospace industry, with some of the top companies by sales (seen in the below graph) experiencing a combined loss of $94.5b in revenue from 2019-2020 and a $2.1b drop in EBITDA over the same period.

As can be seen from the above graph, companies that were more diversified from commercial aerospace markets fared more successfully in 2020. This was especially true of those companies with a focus on defence markets, such as Lockheed Martin and BAE. Another area more resilient to the pandemic was the airline freighter market, which became busier over the pandemic, increasing demand for passenger to freighter conversions.

Looking forward

March 2021 saw a bump in utilisation of the commercial fleet, this was driven by an easing of recent lockdown restrictions in China and increasing travel demand in North America as the vaccine programme continues to run.

U.S based airlines have also started to indicate that they are seeing the beginning of a recovery. Southwest and American Airlines plan to have their whole fleet flying by the summer, domestic US leisure bookings are expected to rise to 90-100% of 2019 levels in mid-year and longer-term bookings, reflecting a growing confidence in the long-term outlook for travel, are also coming in.

Despite these encouraging signs international travel and business travel are expected to lag in recovery, with some airlines suggesting they will not see a recovery to 2019 levels for business travel for many years (2025+).

Our supply and demand model supports some of these preliminary signs. The model forecasts that overall commercial aerospace traffic (in terms of hours flown) will return to 2019 levels by late 2023, with domestic traffic recovering in 2023 and international travel recovering in 2026.

For more information on the market and detailed forward forecasts contact us today.

Sources:

International Civil Aviation Organisation (2021). Effects of Novel Coronavirus (COVID-19) on Civil Aviation: Economic Impact Analysis

International Civil Aviation Organisation (2021). COVID-19 Air Traffic Dashboard.

Boeing Commercial (2021). Orders & Deliveries

Airbus (2021). Orders & Deliveries: Latest Commercial Aircraft Figures.

Airline financial statements and quarterly updates

Aerospace & Defence company statements and quarterly updates

Comments